The nation’s capital played host to a vibrant evening as The LEAD unveiled its Fall Issue just ahead of SmileCon. The room was alive with energy—smiles everywhere, powerful stories in every corner, and leaders from across dentistry coming together with unmistakable purpose.

Executives, clinicians, entrepreneurs, and emerging talent filled the space, creating an atmosphere where ideas moved freely and connections formed effortlessly. The evening embodied what makes The LEAD distinct: elevated experiences, meaningful relationships, and a shared commitment to shaping the next era of dentistry.

By Brian A. Colao Director, DSO Industry Group at Dykema

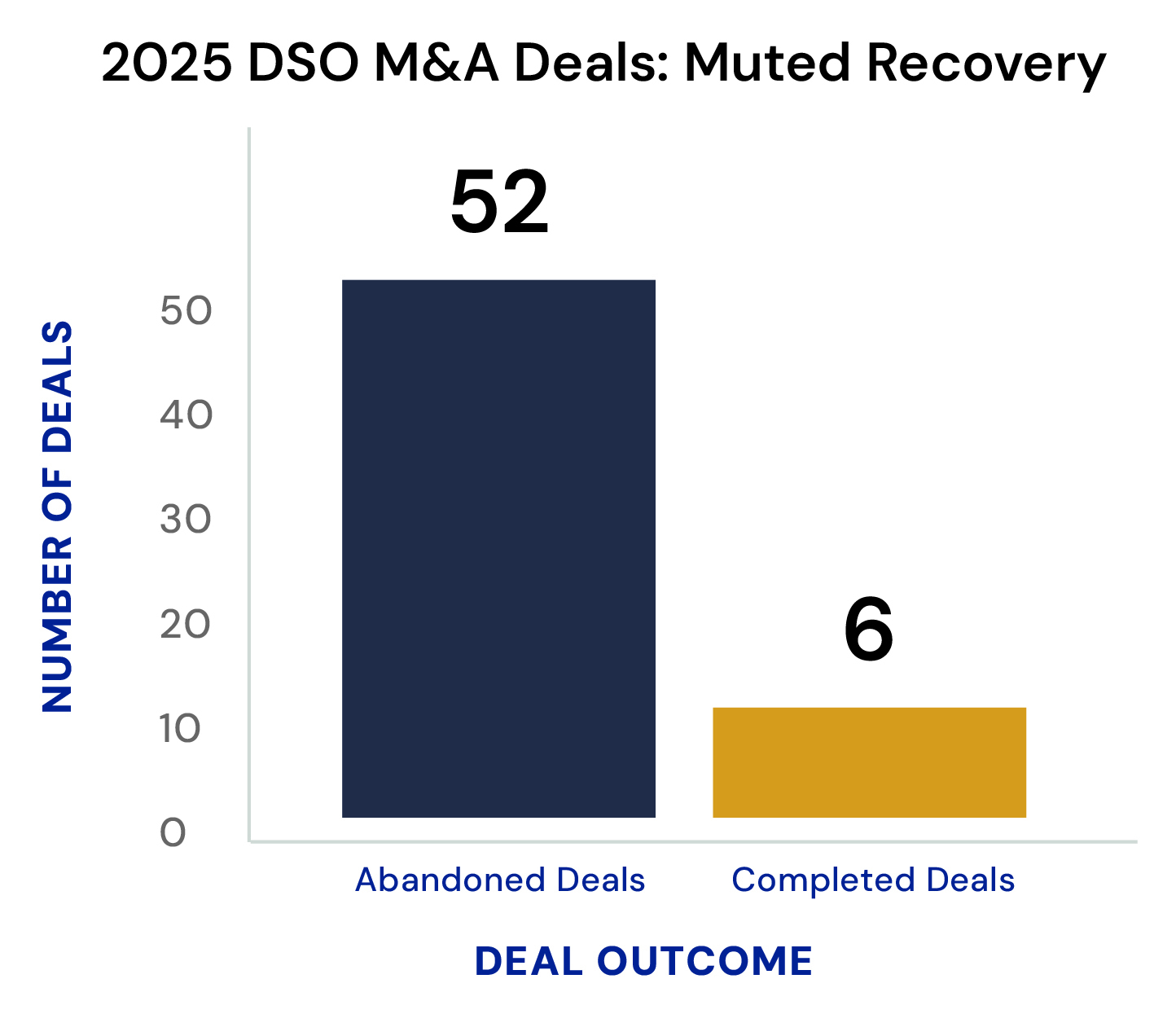

The year 2025 will be remembered throughout the DSO industry as The Year of the Muted Recovery. Entering the year, hope was high that the M&A drought and challenging conditions that began in mid-2022 and caused over 50 significant DSO sales processes to be abandoned would finally subside. A succession of interest rate cuts in late 2024, the inauguration of a new presidential administration promising pro-business reforms, and signals of economic stabilization and the promise of an end to a number of global military conflicts gave rise to expectations that the DSO M&A markets would make a robust rebound.

In my previous year-end article, I identified the critical conditions necessary for a true market revival: sustained interest rate reductions, moderation of inflation, resolution of global unrest, and a regulatory environment that fostered business growth. I also projected that DSOs would increasingly focus on technology adoption for same-store growth to drive EBITDA, compensating for muted acquisition activity.

The Reality: A Muted M&A Market

Unfortunately, virtually none of the foundational pillars for recovery materialized. In 2025, interest rates remained stubbornly high; inflation— though improved—never fell below the key 2% threshold; economically crippling tariffs were introduced against most of the developed world and, as of the time of this writing, much uncertainty remains as litigation over the validity of tariffs appears headed to the US Supreme Court for a decision sometime in 2026. Additionally, the military conflicts in Ukraine and the Middle East have not concluded and continue to exert downward pressure on global markets.

The administration, despite its business-friendly posture, has targeted healthcare fraud aggressively, fueling a notable spike in federal enforcement actions and producing further headwinds for DSO deal-making, which is the subject of a separate article contained herein by my partner, Leigha Simonton, former US Attorney for the Northern District of Texas. As a result, M&A volume remained extremely limited, valuations were pressured, and many groups opted to focus inward, delaying growth decisions and focusing on operational efficiency.

Signs of Hope for 2026: The Year of Renewed Opportunity

Despite these frustrations, several positive signals have emerged, setting the stage for potential improvement in 2026—The Year of Renewed Opportunity:

The Federal Reserve at its Sept. 16 meeting, finally, in a highly anticipated move, reduced interest rates by a quarter point. As of the time of this article, there is optimism that there will be additional rate cuts in 2025 and into 2026 because it will take several more rate cuts to create truly favorable economic conditions for the M&A markets.

Preliminary peace talks in Ukraine and calls for resolution in the Middle East offer guarded optimism regarding global stability.

Legal challenges to tariffs may result in their invalidation, potentially easing supply costs and reducing inflation.

Sellers are increasingly adopting pragmatic valuation standards, acknowledging the need to turn investments amid evolving market conditions.

There have been at least two significant transactions that have closed and several potential transactions that, as of the time of this article, are under Letter of Intent (LOI) and there is cautious optimism that several closings will be announced before year-end, which represents at least a muted recovery with the chance for a fullblown recovery in 2026.

Given these developments, I anticipate an uptick in M&A activity beginning in the second half of 2026, with the potential for momentum to accelerate should economic circumstances and policy frameworks finally align.

A New Era of Healthcare Enforcement

By Leigha Simonton, Former High-Level DOJ Official and Leader of Government Investigation and Defense Practice for Dykema’s DSO Industry Group

This year has ushered in a markedly elevated threat landscape for health care businesses. The US Department of Justice (DOJ) has prioritized healthcare fraud enforcement at an unprecedented level, shifting its approach from isolated financial disputes to aggressive criminal prosecution in cases that, in prior years, might have remained civil contract matters.

This effort accelerated following the DOJ’s May announcement identifying healthcare fraud as a top priority. New initiatives include financial incentives for whistleblowers to report offenses spanning federal benefit programs, private insurer schemes, and a broader array of conduct now categorized as “fraud,” including actions impacting patients, investors, or other nongovernmental entities. The DOJ reinforced its commitment with new dedicated teams, collaborative working groups with HHS, and the launch of the Health Care Fraud Data Fusion Center—a sophisticated operation leveraging advanced analytics and AI to identify emerging fraud schemes.

“The risks of proceeding without expert guidance have never been greater.”

June 2025 saw the largest healthcare fraud takedown in American history, with criminal charges brought against 324 defendants—including nearly 100 licensed medical professionals—for allegedly orchestrating $14.6 billion in fraudulent activity. Notably, this crackdown involved coordination with 12 State Attorneys General’s Offices and extended beyond federal payer fraud to include wire and mail fraud charges associated with private payers, demonstrating a wide net of enforcement.

Given this aggressive climate, industry participants must maintain rigorous compliance and seek experienced counsel with deep knowledge of the DSO industry, government agency processes, and the structuring of advertising, marketing, business development, patient incentive, and compliance programs—and certainly at the earliest indication of possible scrutiny or an internal concern. The government’s sophisticated investigative approach means that even seemingly minor abnormalities can escalate quickly, and the risks of proceeding without expert guidance have never been greater.

Technology: The Imperative of Innovation

Just as predicted, technology adoption for same-store growth has become essential. DSOs nationwide have piloted—and increasingly implemented—innovations in diagnostic AI, cloud-based practice management, automated RCM tools, patient finance solutions, and specialty integration platforms. While adoption has advanced more slowly than hoped—primarily due to challenges in education, training, integration, and implementation—it is steady and inexorable.

Rising costs for labor, supplies, and equipment, combined with stagnant reimbursement rates, have made technology the only viable solution for sustaining margins and driving growth.

A Bright Spot: The 2025 Dykema Definitive Conference for DSOs Amid an otherwise stagnant year, the Dykema Definitive Conference for DSOs emerged as the industry’s true highlight and north star. With attendance surpassing 2,500 and experiences selling out within just hours, the event reaffirmed the strength and future promise of the DSO community. Breakouts and workshops quickly reached standing-room only, underscoring the appetite for practical insights and forward looking strategies. The conference also shined a spotlight on industry leadership: Bob Fontana (The Aspen Group) and Stan Bergman (Henry Schein) received the Lifetime Achievement Award, while respected voices like Dr. Sulman Ahmed (DECA Dental) and Steve Bilt (Smile Brands) reinforced their commitment to advancing the profession.

Just as significant, vendors and sponsors showcased innovations that will help power a new era of growth—advancements that align directly with the industry’s need to innovate, refine operations, and prepare for the rebound ahead. The conference made clear that while recovery may take longer than hoped, the foundation of innovation, leadership, and community is firmly in place to carry the industry forward.

Strategic Outlook: Thriving in Uncertainty

As The Year of the Muted Recovery draws to a close, DSOs must remain strategic and resilient. The best-run organizations will not simply survive the volatility; they will use this period to innovate, refine internal operations, and position themselves to lead as the market rebounds.

My prediction: 2026 will begin with the same cautious progress but, as the year unfolds, will reward those organizations who are prepared—operationally flexible and technologically advanced—when true recovery gains traction. With strategic adaptation and forwardthinking investment, DSOs will be well-positioned to lead dentistry’s next era of growth.

Many dental offices manage waterlines blindfolded: dump in treatment products, test sporadically, and hope for compliance. But waterline safety isn’t just a clinical detail—it’s a litmus test for leadership. Reliable waterline testing reveals more than bacteria counts; it exposes the strength of a practice’s discipline, accountability, and patient-first values. In an era where a single outbreak can shatter brand equity, erode investor confidence, and damage leadership credibility, treating waterline testing as a core key performance indicator (KPI) separates the organizations that scramble from those that lead.

Some argue the cost of compliance outweighs the risk of penalties. But that perspective collapses when you factor in the true cost of reputational damage and litigation. In 2016, one pediatric dental group learned this the hard way after an outbreak linked to contaminated waterlines resulted in 71 confirmed infections, 49 probable cases, and more than 200 lawsuits— an incident estimated to cost tens of millions.

But it doesn’t have to be this way.

There are large DSOs hitting waterline compliance rates well above 95%. That’s not luck. It’s the result of empirically driven, well-built water management protocols that allow waterline testing to shift from a reactive headache to a strategic KPI. High pass rates aren’t just about ticking regulatory boxes; they offer a window into the health of the entire operation.

When DSOs start proactively treating waterline testing as a KPI, they unlock powerful insights into their training effectiveness, operational discipline, and compliance culture at a team and organizational level.

Treatment Isn’t Enough— Test or Risk It

While roughly 75% of offices actively treat their waterlines, fewer than 25% test them. That’s a dangerous disconnect. Regulations require meeting a 500 CFU/mL bacterial threshold. Treatment alone isn’t a guarantee; without testing, there’s no way to confirm the treatment worked.

“Laws and regulations are created because the mass population is not following best practices and guidelines. Those who understand testing is doing the right thing for the patients are the early adopters, starting processes long before they are forced,” Kendra Flowers, a clinical operations/ compliance leader, says.

“Waterline safety isn’t a checkbox — it’s a competitive advantage.”

Many waterline test failures come down to simple, preventable oversight, like forgetting to add a treatment tablet or neglecting in-line filters on ultrasonic scalers. These small gaps often fly under the radar until a failed test forces attention.

Water quality KPIs should be treated like spore testing: nonnegotiable and high stakes. “Unsafe water has deadly consequences,” Flowers says.

The key? Integrate waterline data into dashboards, reviews, and incentive programs. What gets measured—and rewarded—gets done.

Training That Shows Up in Every Test Result

Waterline test results don’t just measure bacteria—they measure training. When pass rates are consistently high across locations, it’s a strong signal that teams are intentionally following protocols.

According to Flowers, high failure rates are common during the initial implementation of a dental waterline protocol. The failure rates reflect the lack of standardized processes, such as:

Heavily occluded lines requiring replacement

Elevated bacterial levels from municipal sources

Staff unfamiliar with proper procedures

Over time, as the protocol becomes embedded in daily operations, staff gain greater awareness, adopt best practices to prevent failures, and consistently follow maintenance routines.

“Protocol makes or breaks waterline safety. We’ve tested hundreds of thousands of samples, and the truth is simple. Every product can work, and every product can fail if protocols slip. With the right training and site-specific procedures, the majority of failures never have to happen,” says Brianna Niederschulte, President of Agenics Labs.

In short, high scores are proof that the training stuck. Use top-performing offices as a blueprint and treat low pass rates as flashing signs for retraining or standard operating procedure (SOP) overhauls.

Onboarding Passes the Ultimate Test

Waterline test results also serve as a real-time gauge of new hire readiness. When DSOs walk every new hire through SOPs in detail from day one, they sharpen accountability and drive better results. If waterline scores dip after onboarding, it’s time to tighten the process—and make sure new hires aren’t just trained but battle-ready.

To assist in new hire readiness and better results, Agenics Labs provides customized onboarding and training for DSOs, including developing and maintaining SOPs.

“Not only does this allow us to provide DSOs with solutions we know will work, but it also means we can work right alongside their practices, helping staff adhere to the group’s established procedures,” says Niederschulte.

Celebrate Your Champions

When offices proactively test and maintain waterlines without reminders, it reveals a culture of discipline and pride in clinical excellence.

“I like to identify champions in all areas of focus or initiatives I oversee,” Flowers explains. “Showcasing the team’s best practices, whether through a company newsletter, peer training for new offices, or coaching support for underperforming teams, not only drives broader adoption of effective strategies but also fosters the development of future leaders within the organization.”

Average DSOs comply because they have to, while great DSOs embed infection control into their operations because giving their patients the greatest care possible is their standard. Recognize and reward the teams that use best practices. Then, use their success to inspire others and embed a culture where accountability isn’t just expected. It’s celebrated.

A Hidden Indicator of Employee Burnout

If well-trained teams are still failing waterline tests, it’s often a red flag for deeper operational issues like understaffing, burnout, or lack of support. This reflects breakdowns in communication, resources, or trust between staff and leadership.

“Most issues turn out to be workflow inefficiencies requiring coaching or protocol tweaks. But when real resource gaps arise, it’s critical to escalate and engage leadership to find solutions,” Flowers emphasizes.

Use low pass rates as a trigger to reassess staffing, redistribute duties, and provide targeted support before small cracks become big problems.

Compliance as a Strategy, Not a Scramble

By adopting the most rigorous, yet reasonable, waterline testing protocols across all states, organizations can create a consistent standard of care and sustainable compliance culture.

“This approach not only mitigates risk but also positions the organization ahead of regulatory changes, ensuring readiness and reinforcing our commitment to patient safety and compliance,” Flowers says.

But protocols alone don’t cut it.

“For any system to succeed, it must be fully integrated into daily workflows, routinely measured, and supported by clear accountability,” Flowers adds.

That’s where deeper, more informative testing can make the difference. Equipping teams with the knowledge to understand what their results mean allows them to take ownership of the process.

“Our mail-in tests include additional water quality metrics that not only help us understand why a sample may have failed but also empower dental team members to identify their own protocol gaps. We are the only lab in the industry to include these extended metrics in every mail-in test, demonstrating our commitment to being comprehensive—one of our core values,” Niederschulte says.

Without this level of integration and insight, compliance becomes a scramble, not a strategy. The best DSOs embed waterline management into the daily routine, track it relentlessly, and use detailed data to prevent failures before they happen.

“Embedding waterline results into dashboards, onboarding, and incentives creates a system-wide feedback loop that builds trust with patients, investors, and regulators.”

Benchmarking That Drives Results

Waterline compliance data isn’t just numbers. It’s a spotlight on which offices are excelling and which need help. By centralizing test results, DSOs can benchmark performance (and check compliance culture) across locations, identify top performers, and replicate their success.

“In addition to our online reporting hub, we curate customized reporting for DSOs, allowing them to view their test data in a variety of ways that can be leveraged for insights into their different locations and collective performance as an organization,” Niederschulte says.

The best teams pass on the first try, no hand-holding required. Their secret? Simple, consistent habits like daily maintenance logs, visual checklists, and operatory signage.

When shared through coaching, newsletters, or onboarding, these practices fuel a culture of compliance and improvement. This isn’t just about tracking—it’s about setting the pace.

Lead the Charge or Get Left Behind

When waterline safety becomes a core KPI, DSOs don’t just check boxes. They drive real, measurable excellence.

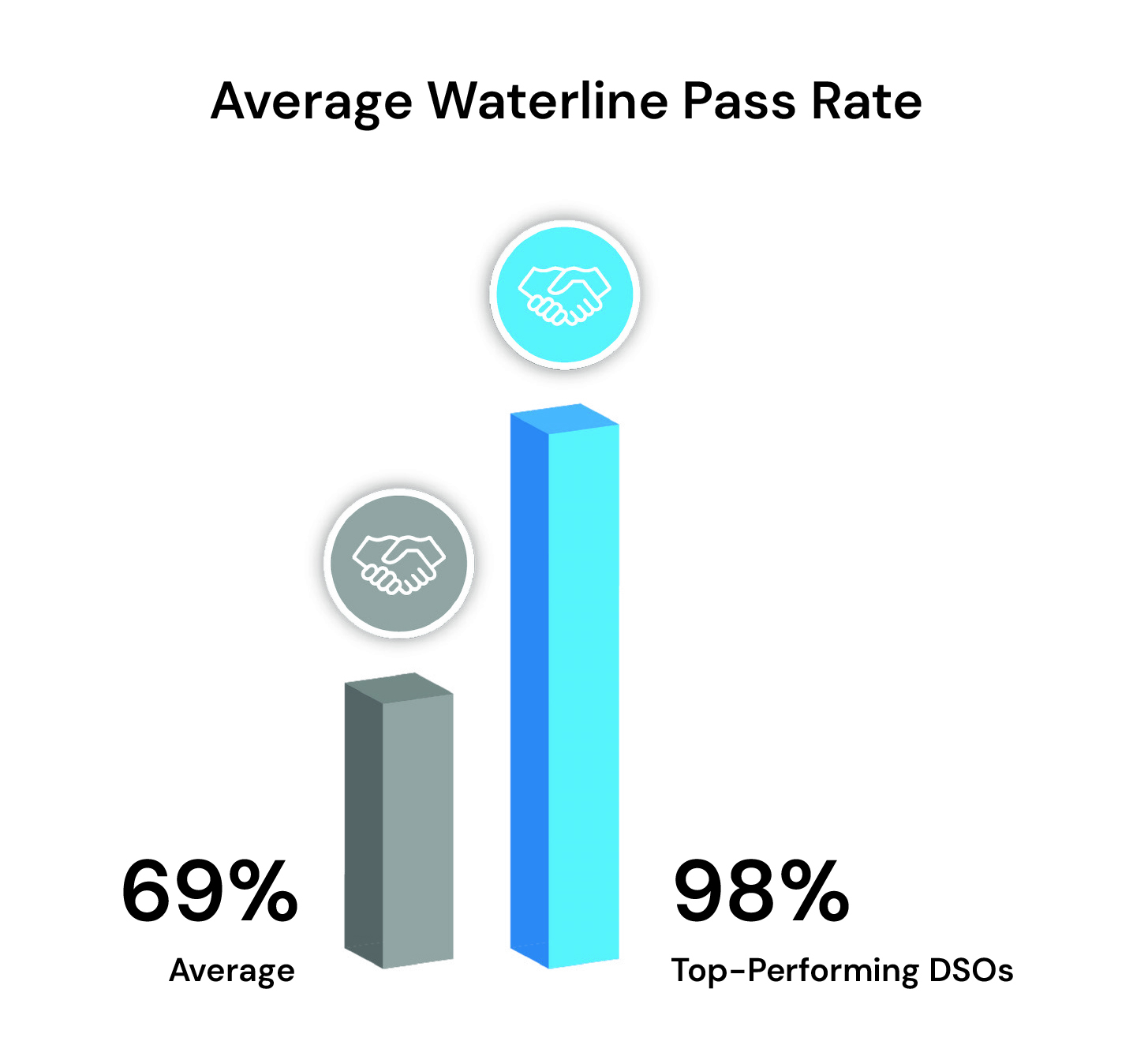

“Two factors consistently drive reliable waterline outcomes: first, standardized protocols tailored to the organization and second, ensuring teams understand the why behind waterline management through meaningful education. When both are in place, we routinely see offices jump from the industry average of around 70% pass rates to exceeding 95%,” Niederschulte explains.

Waterline safety isn’t a checkbox—it’s a competitive advantage. For DSOs, every test is more than a compliance measure; it’s proof of operational discipline, staff readiness, and patient-centric leadership.

The groups that test, not just treat, demonstrate to patients, regulators, and investors that they put safety and accountability first. Those are the DSOs that will earn trust, scale with confidence, and lead the industry forward. The challenge is simple: Use waterline testing as your gauge. It won’t just tell you if your water is safe—it will tell you if your organization is built to win.

Sources:

Ross, Erin. “Infection Outbreak Shines Light on Water Risks at Dentists Offices.” NPR, Average Top-Performing DSOs September 30, 2016.

For most of dentistry’s history in the U.S., being a practice owner was an essential part of being a dentist. The traditional career path was clear: graduate, associate with an established practice for a few years, and then buy in or build a practice of your own. Practice ownership was the marker of success and stability. Most dentists still follow this path. But for younger dentists, the timing of when they get into practice ownership has shifted.

For decades, the American Dental Association has surveyed the U.S. dentist workforce to collect information about their occupation (including ownership status) and basic demographic information. We use the term “practice ownership” here to include dentists who fully own their own practice as well as those who are partners or shareholders in other practice types, such as group practices and dental support organizations (DSOs).

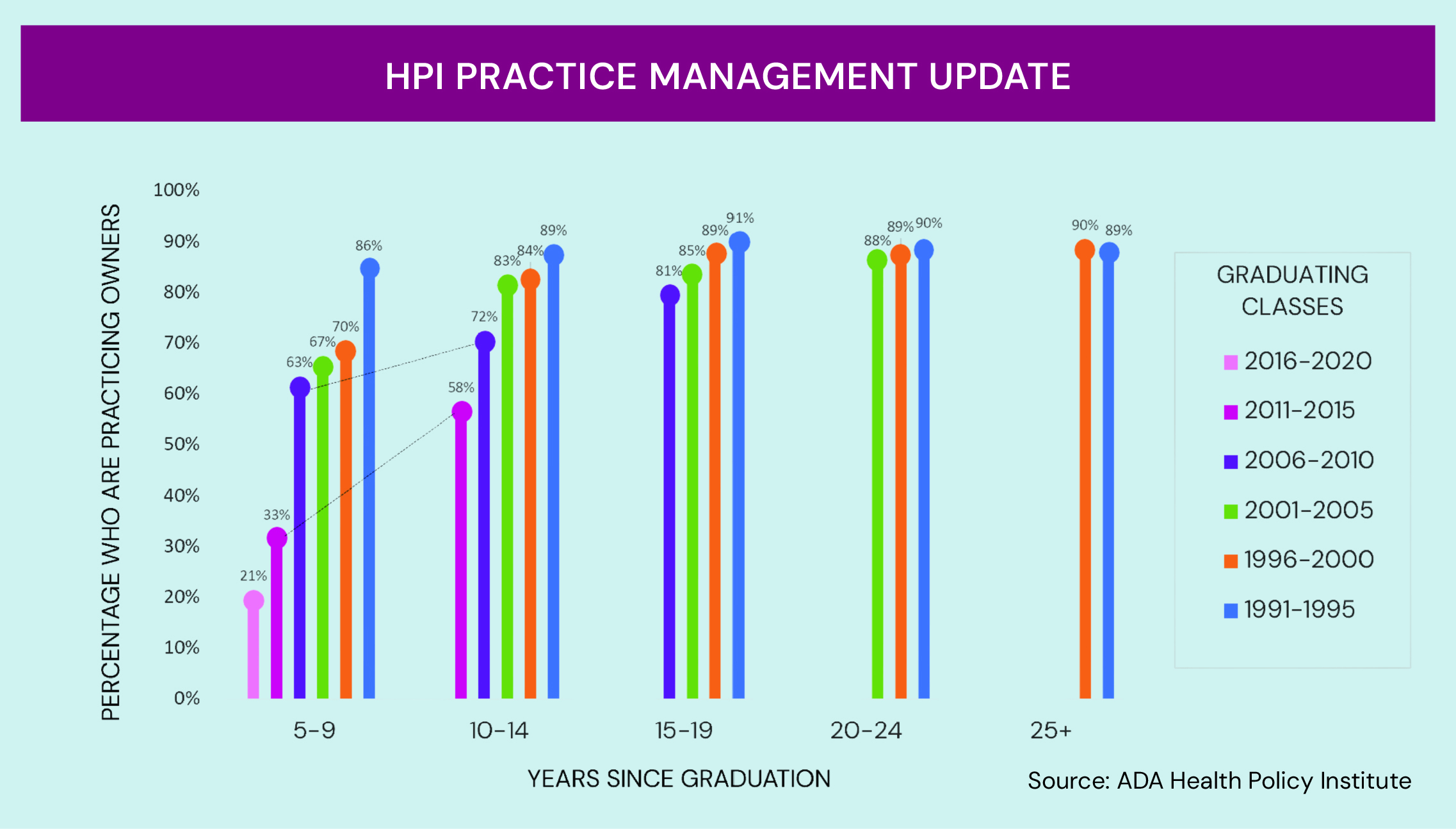

To get a better understanding of how practice ownership has played out for dentists generationally, we looked at survey data from over 55,0000 unique dentists who graduated from dental school between 1991 to 2020 and reported ownership status at least once in their career. To track practice ownership over the career span, we grouped dentists into six graduation cohorts, starting with the classes of 1991-1995 and ending with the classes of 2016-2020. We then looked at practice ownership rates at different career stages for each of these cohorts.

Dentists who graduated from dental school in the early 1990s through the early 2010s show strikingly similar patterns in practice ownership. For these cohorts, ownership was achieved relatively quickly. By the time they had completed their first decade in the workforce, more than three out of five dentists who graduated in the early 1990s through 2010 were practice owners. Although dentists who graduated before 2006 were more likely to be owners at the very early career stage, by the 15 to 19 years of experience stage these differences narrow. The practice ownership rate was 89% for the 1991-1995 cohort compared to 81% for the 2006-2010 cohort.

By contrast, dentists graduating in 2011 or later are following a very different career trajectory than their predecessors. While 63% of dentists from the 2006-2010 graduating classes were owners five to nine years out of dental school, only 33% of the 2011-2015 graduating classes were owners at the same career stage. Thus, there is a significant decline in practice ownership rates in the early career stage for newer graduates. However, as these newer graduates move into the next career phase, their practice ownership rates catch up to their predecessors.

There is a significant decline in practice ownership rates in the early career stage for newer graduates.

Gender adds yet another layer to the story. Across all graduation cohorts, and all career stages, men are more likely than women to own a practice. The gender gap is largest in the early career stage, and then gradually diminishes toward the later career stages. For the newest cohorts of dental school graduates, the rate of ownership for men was 30% compared to 14% for women early in their careers. One thing to note is that while the levels differ, the shapes of the trend lines across the career span are similar for both genders. Practice ownership generally rises over time but starts at a much lower level for more recent graduates.

Why is practice ownership in the early career stage dropping for younger dentists? While there is no definitive research, we think several forces are at play. Educational debt might steer new dentists away from pursuing practice ownership right out of the gate. Some younger dentists may value flexibility or reduced administrative burden and may not see ownership as immediately appealing or conducive to work-life balance. The changing demographics of the dental workforce, where now the majority of dental school graduates are women, is another factor at play.

While men and women follow similar paths, women start at a far steeper climb toward ownership.

While some version of practice ownership still seems to be the end point for most dentists, it is clearly no longer the quick step it was a generation ago. We also caution that for the newest cohort of dental school graduates we have only limited data—for the first 10 years of their career. There is clearly something quite different about this cohort, and it remains to be seen if their “catch up” rate is indeed as quick as the cohort before. We will update the data as they become available. Stay tuned.

On August 6th, the Gaylord Resort in Denver came alive as leaders across dentistry gathered for The LEAD Fall Release Party. The evening was a celebration of powerful stories, inspiring women, and aspiring leaders. We honored the partners who make our mission possible—visionaries whose influence is shaping the future of dentistry.

In a moment of gratitude and recognition, The LEAD presented seven distinguished awards to honor industry pioneers and partners whose contributions continue to elevate the profession. From long-term allies to rising stars, these honorees embody the spirit of leadership, innovation, and impact.

The movement grows stronger. Join us on October 22nd, 2025, in Washington D.C. for another unforgettable evening as we celebrate the next chapter and fall edition of The LEAD.

Vyne Dental’s Chief Product Officer Paul Bernard explores how leading DSOs identify, measure, and fix these gaps—and how you can too.

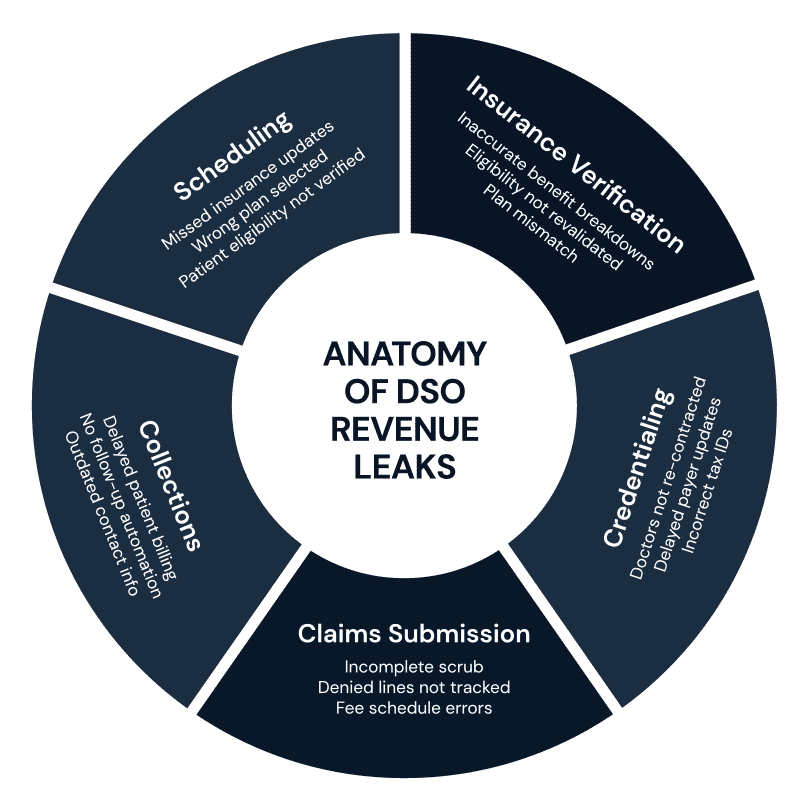

Many DSOs unknowingly lose thousands of dollars to inefficiencies hidden deep within their revenue workflows. From inaccurate coding to outdated collection processes, these “invisible leaks” can significantly impact the bottom line.

Whether you are running 50 offices or one, the RCM process is the same. However, the law of large numbers begins to affect DSOs as they grow.

“Every practice leaks, but these leaks really start showing up in a more magnified way the bigger you get,” Vyne Dental Chief Product Officer Paul Bernard says. “At the end of the day, if you see a patient and you expect to be paid $100, how much of that do you actually put in your pocket—and how much effort does it take to get those final pennies?”

Start with a Bigger Bucket RCM starts long before billing a claim. The work you do up front to build a successful claim is part of the process. “People tend to want to bucket RCM too small. They think RCM is just billing the claims, which is just one piece. The whole process, from scheduling a patient to the patient making their final payment and everything in between, has aspects that significantly impact RCM,” Bernard explains.

By investing time on upfront processes in RCM, you can avoid spending energy on cleaning up mistakes. A process map can help you visualize that.

“Process mapping is not intuitive for a lot of people, but it’s no more complicated than examining what happens first, and then what happens next. You’ll start to see that prep work matters. It’s everything that happens before filing that makes that claim successful or not successful,” says Bernard.

Beyond mapping, narrowing your perspective on RCM can also limit your potential improvements.

Every practice leaks. The bigger you get, the louder it drips.

“For instance, some think scheduling has no impact on RCM. It absolutely does,” Bernard notes. “I want to be looking for things at scheduling that will help me submit a successful claim, such as asking if patients have changed employers. Is their insurance still the same? If they don’t know, go ahead and schedule but loop back before they show up to see if you’re in network.

“If you have a narrow view of RCM,” Bernard points out, “you are going to find narrow opportunities to improve. All the things that must happen before you even send a claim to a payer contribute to how much you will be paid.”

Mistakes You Can’t Afford

Incomplete or Delayed Credentialing One way DSOs can miss out on or delay revenue is failing to properly contract and credential doctors. This can significantly impact how and when they are paid.

When DSOs acquire a practice, payers have to be re-contracted, which usually happens under a different tax ID.

“Payers will send payments to a tax ID, not a doctor who’s in a location. Knowingly or unknowingly, you changed where the money gets routed, and your processes in RCM have to adjust for that,” Bernard explains. “Those claims won’t get paid because the insurance company doesn’t know who this doctor is. You’ve billed a claim that isn’t getting paid, and you end up having to unwind problems, which will cause delays in payment or denial of payment.”

Not Mining EOBs Explanations of benefits (EOBs) are a tremendous source of process data because they will tell you what claim got denied, what line on a claim got denied, and why. If you understand those reasons, then you can see where in your process flow you could have caught it.

Inevitably, a lot of errors are going to be at the point where you validate whether the eligibility and benefits are accurate and before you make an estimation and choose a fee schedule. Find and fix that error—and get paid.

“It does you no good if you have a good eligibility and benefit breakdown but you’re picking the wrong plan for that patient. You are never going to get the exact amount correct, so maintaining these plans and payer plans and fee schedules in your practice management system is critical if you want to bring those two together,” Bernard explains.

If your view of RCM is narrow, your results will be too.

Incomplete Claims The ultimate goal is a clean claim with no receivables to manage. “You want to be collecting as much of what the patient owes up front as you can and then have some reasonable certainty that once you send that claim, it’s going to get paid whatever the insurance owes you,” notes Bernard.

“That’s a perfectly clean claim. That would mean that the level of effort that you must spend managing the receivable is zero because there is no receivable.”

Products like Vyne Trellis scrub claims before they get to the payer.

“It’s much better to try and put as much effort as you can up front to make sure that that claim is correct,” Bernard explains. “You can take 10 minutes now to fix it, or you can take two hours 30 or 60 days from now to try and figure out why you didn’t get paid. It’s a no-brainer—and yet somehow, we still allow these defects to escape the process.”

It’s All About Data Don’t worry about making sure everyone is on the same practice management system.

“Why would you take a doctor who is unbelievably productive and generating revenue using whatever system they’ve been using and say, ‘Now that you’re part of a DSO, you need to switch.’?” Bernard asked. “Why would you rip out the wiring from somebody who is usually productive?”

The reality is that forcing a change often results in reduced productivity because staff are unfamiliar with the new system. It introduces unnecessary risk into the operation of a practice that was otherwise performing well.

Instead of focusing on uniformity of systems, DSOs should prioritize access to data. “Insist that the practice management systems give you your data,” he said. “Once you have it, you can bring that data into a centralized system and analyze it however you want. If you can free the data from those systems, you don’t need to change anything—and you reduce your operational risk.”

Once your data is accessible, you can measure performance across the organization without disrupting what Appointment Credentialing Claim Scrubbing Data Errors is already working. It’s not about the system itself—it’s about the visibility and control the data gives you.

Keep the Patient in the Loop “You’ve got to think about the billing experience from the patient’s perspective,” says Bernard. “At Vyne Dental, we call it ‘patient in the loop.’”

If a patient leaves the doctor’s office, hears nothing for weeks, and then a surprise bill arrives, it can prompt confusion, doubt, and a timeconsuming call to the office. What if, instead, they were kept in the loop the whole time with clear, proactive updates? By the time the bill comes, they understand it, trust it, and are far more likely to pay it.

“There’s a direct correlation between time and payment,” Bernard explains. “The older that receivable gets, the less likely it is to be paid.”

When you build a billing process that moves efficiently, it not only benefits the patient but also strengthens the practice.

Prep work matters. It’s everything before the claim that makes it successful—or not.

Build Smarter, Scale Stronger RCM isn’t just billing—it’s a living ecosystem. And like any complex system, it’s only as strong as its weakest link. From initial patient scheduling to the moment a claim hits the payer, every step in the process either protects revenue or puts it at risk.

The most successful DSOs aren’t the ones who work harder to chase revenue—they’re the ones who build smarter systems to prevent loss before it happens. They invest in automation. They map out their processes. They scrub claims early. And they never stop analyzing their EOBs for trends that can unlock even greater efficiency.

Because at the end of the day, your revenue isn’t what you bill—it’s what you keep.

Strengthen your pipeline. Protect your bottom line. Scale with confidence. Experience Vyne Trellis®— the end-to-end revenue acceleration platform that gets you paid faster through streamlined claims submission and tracking, delivers batch and realtime eligibility checks, and keeps your communications secure.

Ready to Stop Revenue Leaks Before They Start? Schedule your personalized demo today at VyneDental.com.

A new generation of dentists is reshaping ownership, gender balance, and affiliations— with long-term consequences for the business of dentistry.

By: Rachel Morrissey and Marko Vujicic

What does it mean to be a “typical” dentist? Twenty years ago, the average dentist was likely in their 40s, midcareer, and the owner of a small practice. At that time, the profession was dominated by baby boomers who had graduated in the late 1970s and early 1980s, an era marked by a surge in dental school graduates.

Today, the picture looks quite different. Over the past several years, a generational shift in dentistry has been taking place, with more dentists at both the beginning and end of their careers. The large cohort of baby boomer dentists is now reaching their late 60s, with retirement on the horizon. At the same time, a growing number of young dentists are entering the field—a pattern that shows no signs of slowing.

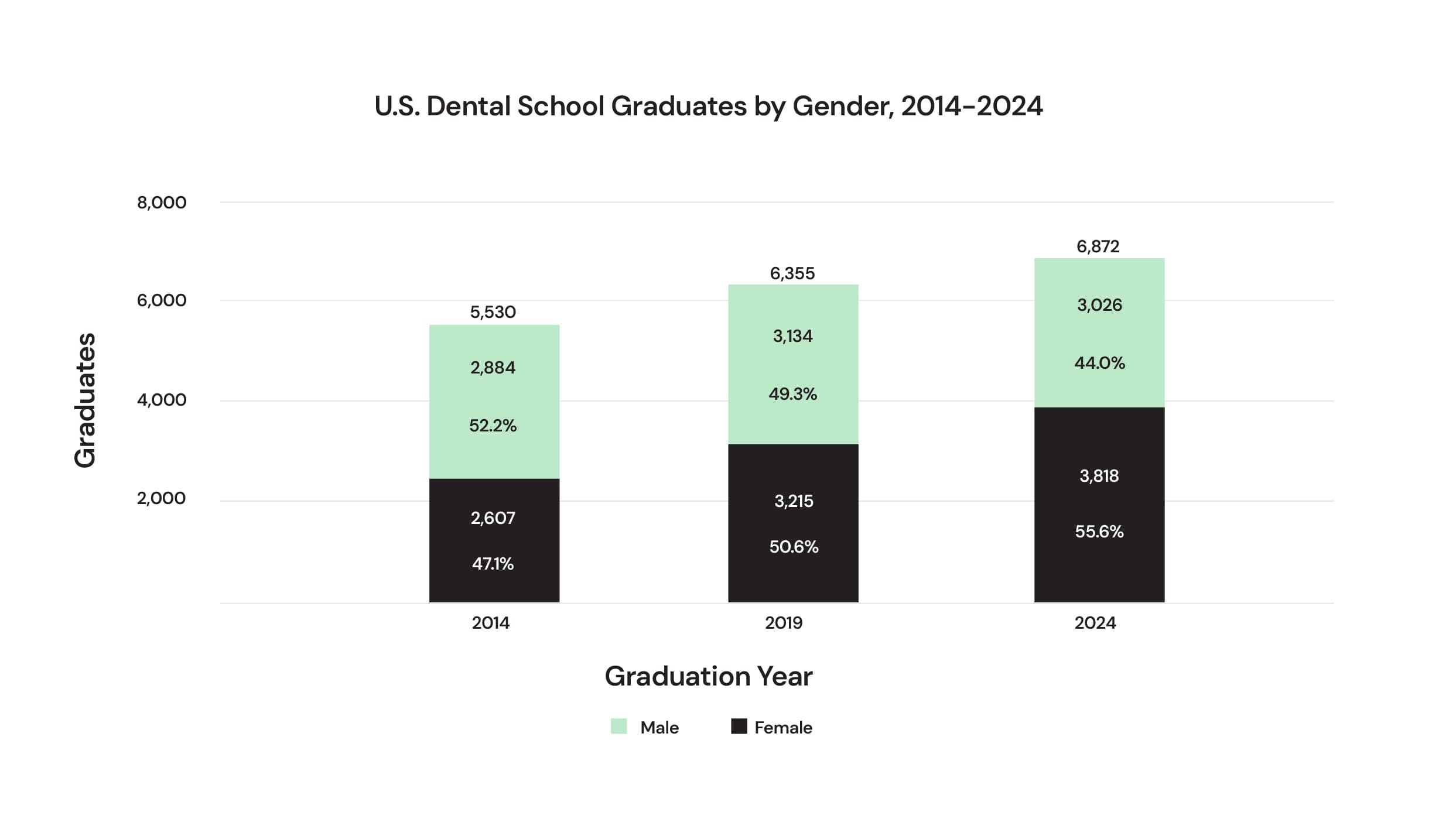

The number of dental school grads in the U.S. has gone up since the early 2000s, following a large drop in graduates that began in the late 1980s. The introduction of more than a dozen new dental schools in the U.S. since 2000 contributed an additional 9,000 graduates to the already rebounding workforce pipeline over the last two decades. Between 2014 and 2024, there were just under 70,000 dental school graduates.

Women now make up 56% of dental school graduates—a figure reshaping the entire profession.

Another major shift in today’s dental workforce is gender representation. In the early 1980s, women made up only about 20% of dental graduates. By the early 2000s, men still outnumbered women in predoctoral dental programs.

That trend has since reversed: Beginning in 2019, women comprised the majority of dental school graduates.

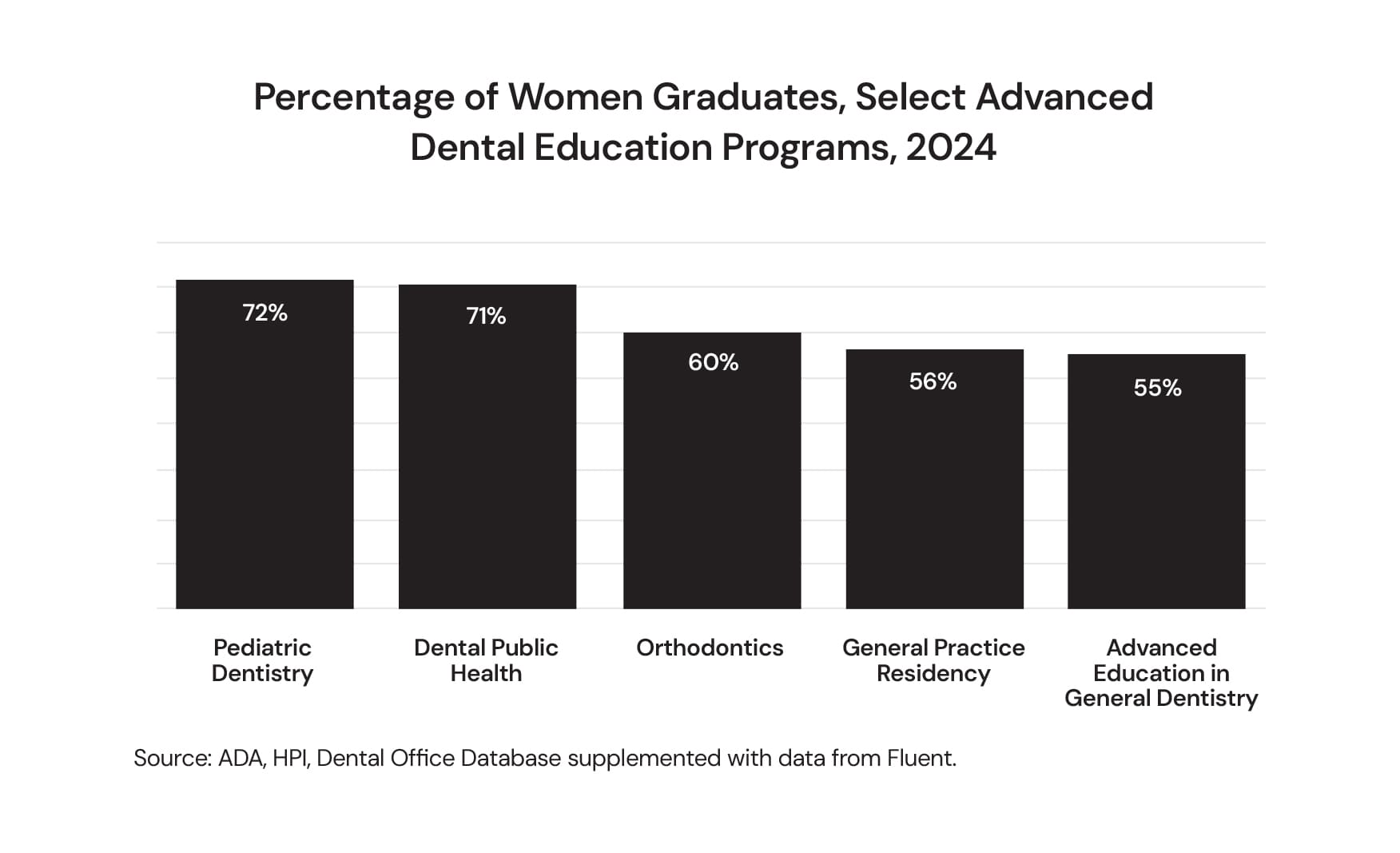

In fact, in 2024, 56% of dental school graduates were women. Women also made up more than half of the graduating classes of several advanced dental education disciplines in 2024, including pediatric dentistry, orthodontics, and general practice residency programs.

Source: American Dental Association (ADA), Health Policy Institute (HPI), Commission on Dental Accreditation Surveys of Dental Education.

What does a younger, increasingly female dentist workforce mean for the future of the profession? One key implication lies with practice modality. HPI has been closely tracking changes in dentist affiliation with DSOs as well as shifts in dental practice size, measured by the number of affiliated locations within a practice. Both aspects of practice modality are changing, and the gender and age shift are major drivers.

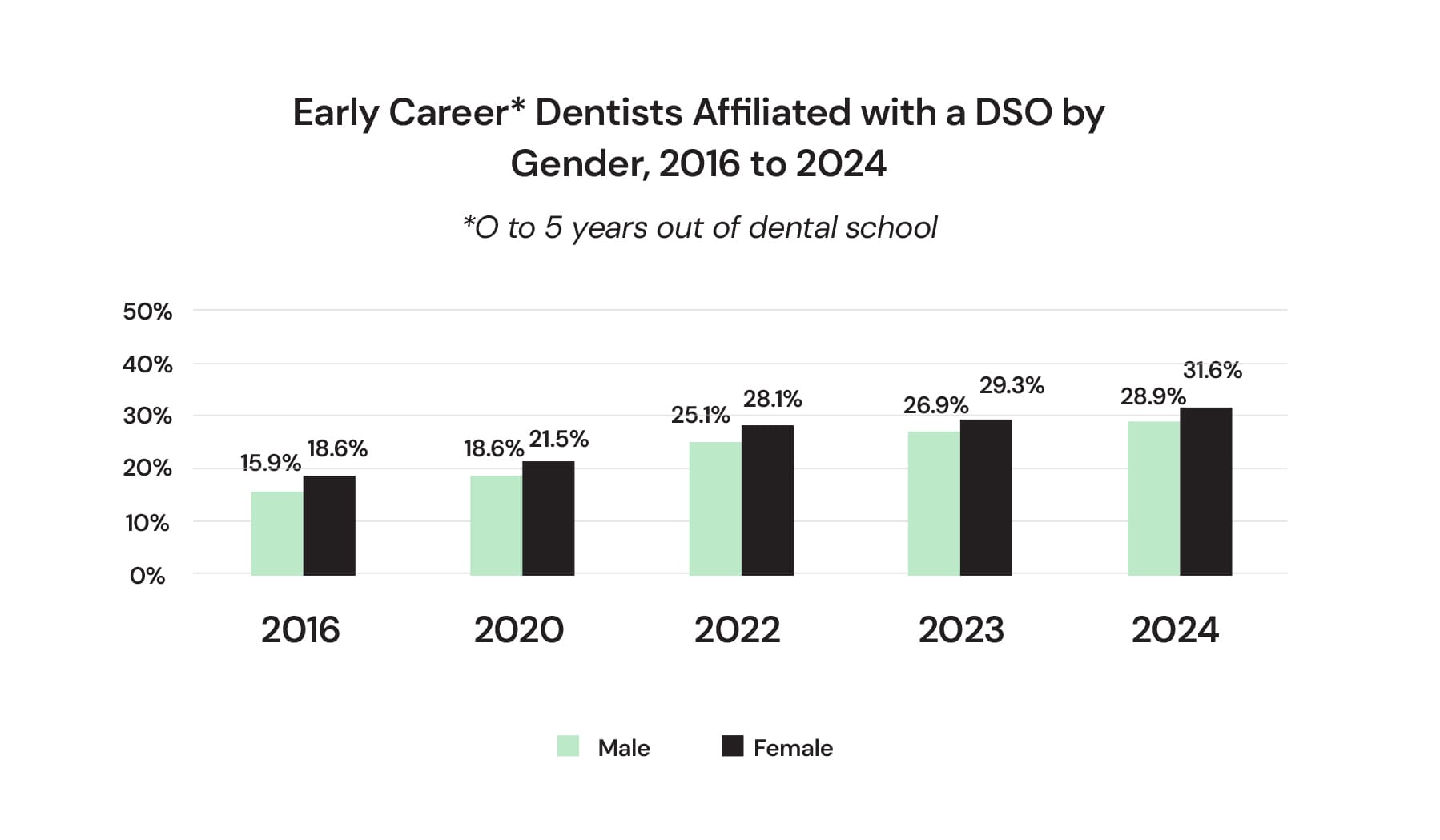

There are major differences in practice modality depending on dentist career stage. Early career dentists are far more likely to practice in larger groups and to be affiliated with a DSO.

As of 2024, one-third of all dentists are in solo dental practice (34%) while less than one-fifth work for a large group practice with 10 or more affiliated locations (17.4%). For younger dentists—those up to 10 years out of dental school—the reverse was true: 15% worked in solo practices compared to 29% in large group practices.

The share of dentists affiliated with a DSO has more than doubled in the last 10 years. In 2024, about one out of every six dentists overall was affiliated with a DSO. While this number has grown for all dentists, it is particularly robust for young dentists, with women even more likely to work at a DSO-affiliated practice. In 2024, close to one-third (32%) of female dentists up to five years out of dental school were in a DSO-affiliated setting.

Increased affiliation with DSOs is not likely to reverse any time soon. The American Dental Education Association’s 2024 Survey of Dental School Seniors showed that 32% of surveyed dental school seniors who plan to go into private practice following graduation intend to join a DSO-affiliated practice. Just five years ago, 18% of dental school seniors reported the same plans, a little more than half of today’s number.

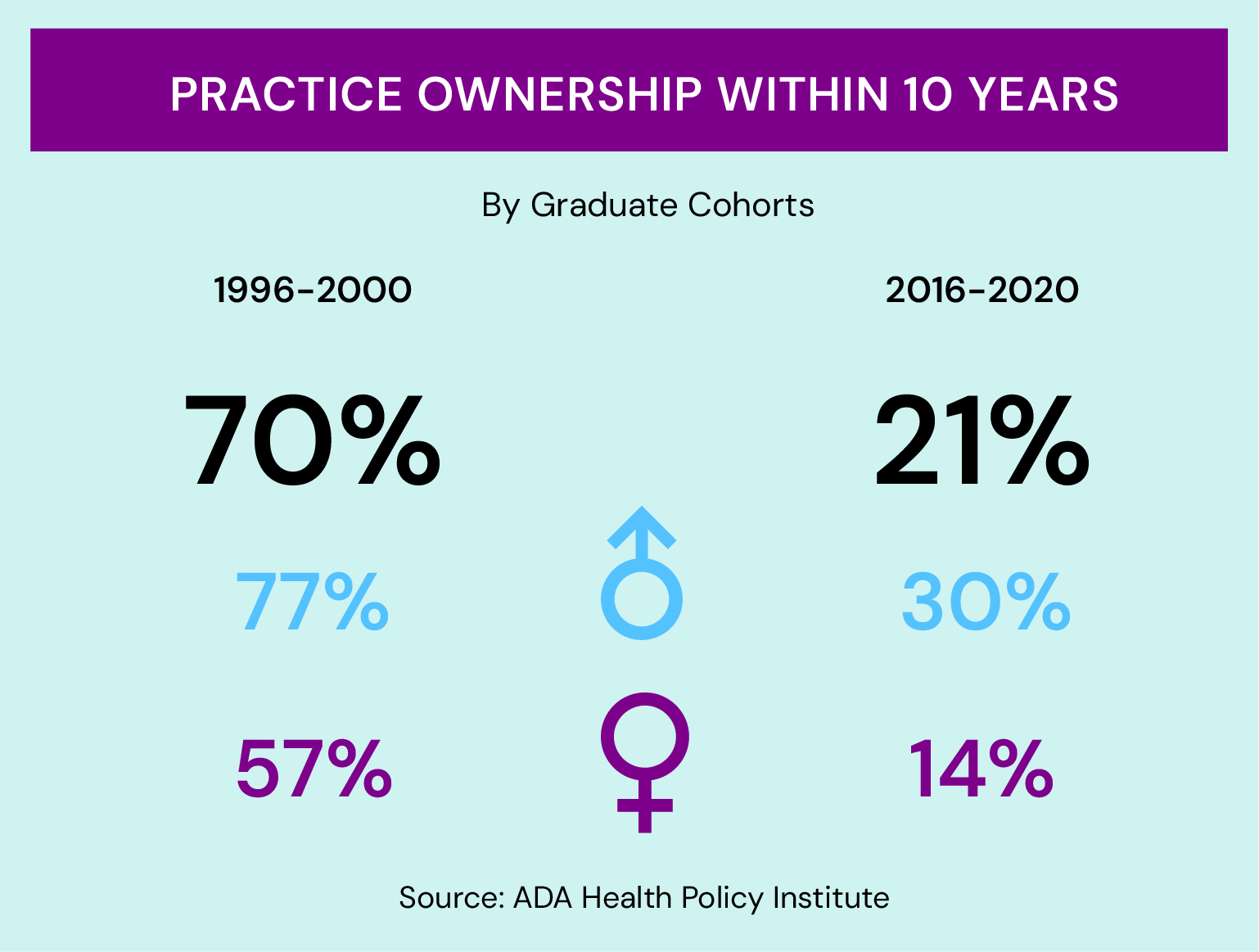

An examination of practice ownership trends reveals a similar pattern of divergent career choices across age and gender cohorts. HPI analyzed data looking at practice ownership at different career stages for cohorts of dentists who graduated between 1991 and 2020. For dentists who graduated in 2010 or earlier, the majority were practice owners five to nine years after graduation. In sharp contrast, only about 20% of dentists who graduated between 2016 and 2020 were practice owners at the same point in their career. For women dentists in this cohort, the figure is 14% compared to 30% for men.

In 2024, nearly one-third of new female dentists joined DSO-affiliated practices.

The demographics of dentistry are shifting. More dentists are choosing career paths in larger group practices or DSO-affiliated settings over traditional solo ownership early in their careers. As this new generation grows, their preferences will continue to redefine what it means to be a dentist today.

Rachel Morrissey is a senior research analyst at the American Dental Association’s Health Policy Institute, where she leads the analysis of data for a variety of projects focused on dental education and emerging issues in dentistry. She has co-authored several articles on the dental workforce, published in Health Affairs Scholar, Dental Economics, and the Journal of Dental Hygiene.

Marko Vujicic currently serves as Chief Economist, Chief of International Relations, and Vice President of the Health Policy Institute at the American Dental Association. He is a recognized thought leader in health care policy as it relates to dental care. He has published extensively in peer-reviewed journals such as Health Affairs, The New England Journal of Medicine, and his team’s work is regularly cited by CNN, The New York Times, The Wall Street Journal, Fox News, and other media outlets. Previously, he was Senior Economist with The World Bank in Washington D.C. where he focused on health systems reform in developing countries.

Confidence Crisis? Dentists Weigh in on the 2025 Economy

03/06/2025

|

4 min. to read

Female Dentists Are More Optimistic.

By Rachel W. Morrissey and Dr. Marko Vujicic

The economic landscape is in a state of flux as of early 2025. From lingering inflation to uncertainty around tariffs and interest rates, the effects are being felt across the health care industry, including dentistry. Since 2022, the American Dental Association’s Health Policy Institute (HPI) has conducted a regular survey of dentists in private practice to gauge their economic outlook for their practices, the dental sector, and the U.S. economy. This ongoing pulse check offers insight into how external economic pressures translate into real-time confidence—or caution—within the profession.

Since HPI began collecting these data, dentists’ confidence in the six-month outlook for their practices and the dental care sector has remained relatively stable. Between half and two-thirds of dentists reported feeling somewhat or very confident in these two sectors since early 2022. Confidence in the outlook for the U.S. economy, while rising steadily over the years, has consistently been lower than the dentistry-related measures.

Reverses in Confidence

At the end of 2024, dentists appeared optimistic about the U.S. economy. Confidence reached its highest level since the poll began, with a majority of dentists (56%) reporting a very or somewhat confident outlook for the coming six months. However, this trend reversed sharply by the end of March 2025, with just over one-third of dentists (35%) expressing the same level of confidence in the near-term economic outlook.

Dentists’ confidence in their own practices and in the broader dental sector remains higher than their confidence in the U.S. economy. Since early 2022, a majority of dentists have reported a positive economic outlook for the dental sector. However, this confidence dipped in the first quarter of 2025, with only 45% of dentists feeling somewhat or very confident in the outlook for their practices—a decline of about 17 percentage points from the previous quarter.

The Gender Gap

Among female dentists, the decline in dentistry-related confidence was less pronounced. Female dentists have consistently reported higher confidence levels in the dental sector and slightly higher confidence in their individual practices compared to male dentists.

Additionally, when comparing female dentists and male dentists, confidence patterns differed. From early 2022 through the end of 2024, female dentists consistently reported higher confidence in the U.S. economy than their male counterparts. In December 2024, while both groups saw an increase in optimism, the rise among male dentists was steeper.

By early 2025, confidence among women dentists had dropped to 34%, with men only marginally higher at 35%.

Falling Consumer Confidence

The decline in dentists’ economic confidence mirrors broader national sentiment and rising consumer pessimism. According to April 2025 data from The Conference Board’s Consumer Confidence Index, consumer confidence has fallen for five consecutive months. Short-term expectations—based on perceptions of business conditions, employment opportunities, and income—have reached their lowest levels since 2011.

Patient Demand: Perception vs. Reality

Consumer caution may already be affecting patient behavior. HPI’s survey tracks dentists’ ability to meet patient demand by monitoring their perceived busyness over the previous three months. In the first quarter of 2025, there was a slight increase in the percentage of dentists who reported being “not busy enough,” rising from 24% to 28% compared to the previous quarter. Dentists working in DSO-affiliated practices were more likely to be busier.

However, other data tell a slightly different story on patient demand. The Bureau of Economic Analysis tracks consumer dental spending. The latest data show that spending on dental services has been trending up slightly through March of 2025. Accordingly, it is still unclear how much the downturn in dentist economic confidence in early 2025 is being driven by a drop in patient demand.

HPI will continue to monitor these trends and share insights as more data become available. In the meantime, tune into the ADA Chief Economist’s take on future trends in the dental care market at the ADA’s Dental Sound Bite podcast.

This party was one for the books. Set in the iconic Caesar’s Palace in fabulous Las Vegas, the evening brought together the dental industry’s most discerning and dynamic leaders. Gowns, tuxedos, sharp suits—it was a room filled with style, presence, and purpose.

A roaring 1920s-inspired band set the tone, blending timeless flair with a fresh vibe. Laughter carried across the room, connections sparked, plates were full, and glasses clinked as we celebrated The LEAD and its impact.

More than launching a new issue, this event marked our one-year anniversary. If you were there—relive the magic. And if you weren’t—let this be your reason to join us next time.

Predictions and Analysis on Economic Conditions, Technology and M&A Trends

By Brian A. Colao Director, DSO Industry Group at Dykema

The last two-plus years have been the toughest economic environment in the history of the DSO industry. The challenges began in early 2021, near the end of the COVID-19 pandemic, with a new presidential administration that flooded the economy with a surplus of aid programs, many of which proved unnecessary. Around a year later, Russia invaded Ukraine, destabilizing global markets, followed by several crises in the Middle East. The result was the highest interest rates and inflation in the history of the DSO industry, coupled with record costs for goods and labor. These difficult economic conditions significantly lowered EBITDA, leaving many organizations struggling to maintain positive cash flow and comply with the terms of their credit facilities. These conditions also caused a massive slowdown in the once-booming DSO M&A markets, creating great uncertainty heading into the November 2024 presidential election.

In November 2024, one of the most closely watched elections in U.S. history took place, resulting in the election of a new presidential administration. Interest rates have since been lowered by the Federal Reserve. This raises the question: what can we expect for the DSO industry in 2025?

Economic Conditions are Trending in a Positive Direction

Going into 2025, there are a number of favorable economic conditions, including the following:

1. The Federal Reserve cut interest rates three times in the latter half of 2024, during meetings in September, November, and December, totaling a full percentage point reduction. This has led to more favorable lending conditions, with expectations that rates will continue to decline throughout 2025.

2. Investor confidence has improved significantly after the outcome of the 2024 presidential election, with the stock market rising more than 1,500 points and 3.6% the day after the election and continuing to rise over the next few weeks.

3. An enormous amount of investor capital remains on the sidelines, waiting for the right opportunities.

4. There is also a large inventory of dental organizations of all sizes that are seeking recapitalization events.

5. Many technological innovations have either come online or are expected to come online soon, which can dramatically improve the same-store growth of dental organizations.

The New Presidential Administration is Expected to Pursue a Much Less Stringent Regulatory Environment

Going into 2025, the regulatory environment appears much more favorable, including the following factors:

• The FTC’s proposed non-compete rule was enjoined by a federal court on August 20, 2024. The new administration is not expected to pursue the enforcement of this proposed rule, which will create much more favorable conditions for the labor market.

• The Corporate Transparency Act was enjoined by a federal court on December 3, 2024. If this injunction is upheld, it will create a less burdensome environment for corporate entities.

• The current FTC director will be resigning, and a new director appointed by President Trump will be taking over with a much more business-friendly philosophy.

• President Trump has pledged to overhaul the Justice Department, which is expected to lead to less aggressive healthcare-related investigations and enforcement actions.

• Governor Gavin Newsom recently vetoed SB 842 (in September of 2024), which, if signed into law, would have allowed the California Attorney General broad powers to block healthcare M&A transactions.

Amazing Innovations Exist to Boost Same-Store Growth for DSOs

This is truly one of the most exciting times in the history of the dental industry. There have been more innovations in the last five years than in the previous 100 years. Some of the most incredible innovations that either exist or are coming soon include:

• Diagnostic AI allows for the diagnosis and treatment of many more dental conditions than ever before.

• AI is automating payment of invoices, adjudication of insurance claims, approvals, collection of receivables, and improving revenue cycle management. AI is also reviewing phone calls to maximize patient retention.

• A revolutionary product exists that has the potential to regenerate enamel and monetize the treatment of minor cavities without resorting to the traditionally invasive “drilling and filling” procedures.

• Membership plans are increasing the ability of dental organizations to attract and retain patients who lack insurance.

• Technological advancements and innovations in clear aligners, implants, anchored dentures, sleep medicine devices, and traveling specialists have made the integration of specialties into general dentistry offices easier than before.

• Innovative patient finance solutions have made access to treatment easier than before.

• Other technology advancements include real-time tracking of capital tables and earn-outs, lease management, management of merchant fees, the use of big data to determine market presence, and lab consolidation—all of which have the potential to reduce overhead.

These technologies can increase same-store growth, lower overhead, and compensate for shortages in clinical and non-clinical employees. However, challenges remain in the adoption of these technologies, including resistance to change, lack of effective implementation plans, and the integration with existing technologies already in use at dental organizations.

Questions and Predictions for the First Half of 2025

There are several key questions as we enter the first half of 2025:

1. Will interest rates go low enough to truly jump-start M&A markets?

In December of 2024, the Federal Reserve Chairman delivered disappointing news, by projecting just 2 rate cuts, down from its original anticipated rate cut of 4. This caused stocks to tumble. The Chairman cited persistent inflation as the main reason for the smaller-than expected reduction, warning that it could take until the third or fourth quarter of 2025 for inflation to improve.

2. Is investor confidence high enough to truly jump-start M&A markets?

Investor confidence is at its highest point in the last three years, and there is significant capital waiting to be deployed but inflation still remains higher than it should be and interest rates will not be reduced as quickly as the market had hoped.

3. What will 2025 valuations for dental organizations look like?

I believe valuations will be fair but not as high as they were at the end of 2020 and 2021, when market highs were reached.

4. What will 2025 deal structures look like?

The market will continue to utilize rollovers, earn-outs, and joint ventures as a means of mitigating risk for transactions into 2025. EBITDA will also be scrutinized much more strictly than it was during the market highs in 2021.

5. What will same-store growth look like?

Organizations that adopt new technologies, properly implement them, and integrate them with existing systems will experience substantial same-store growth.

6. What challenges could derail a market rebound in 2025?

• New wars or global unrest. • The implementation of draconian policies, such as onerous tariffs. • Failure to achieve low enough interest rates. • Stubbornly high inflation.

Prediction for 2025

I predict a gradual recovery during the first two quarters of 2025, with smaller to mid-sized deals closing in this period. I expect to see improved deal activity in the third and fourth quarters of this year, assuming there are no major global or domestic setbacks. Additionally, I anticipate a dramatic increase in the adoption and successful implementation of new technologies in 2025, which will lead to significant same-store growth for dental organizations.